Omnibus Legislation: What Does It Mean for the CSRD?

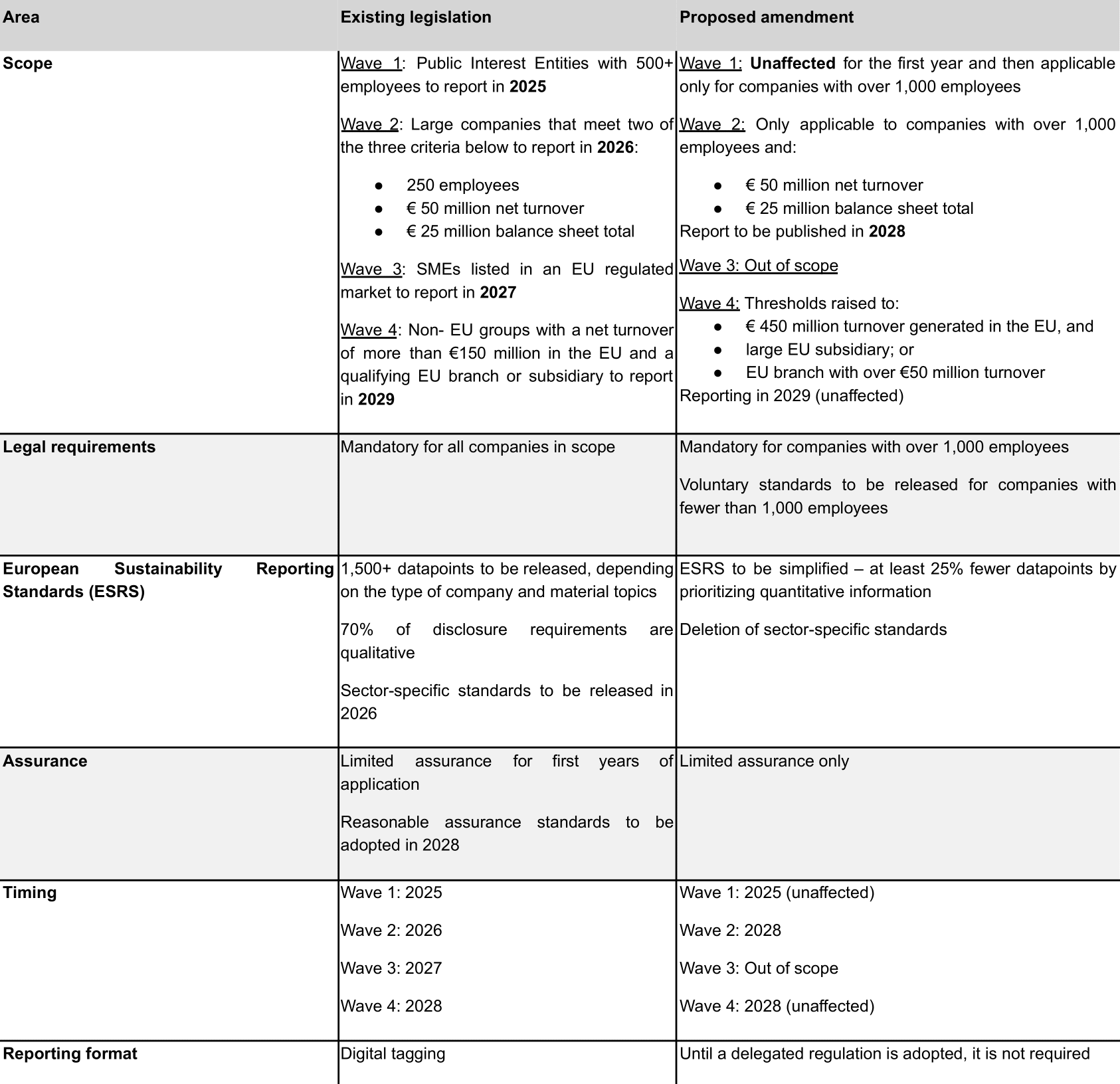

Comparison between the existing legislation and the proposed amendment

The Omnibus package was proposed by the European Commission on 26 February with the aim of simplifying ESG rules and making EU businesses more competitive. The package, if adopted, will reduce administrative burdens for all companies by 25% and for SMEs by 35%.

What will the legislation do?

Omnibus impacts the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), EU Taxonomy and Carbon Border Adjustment Mechanism Regulation (CBAM).

Regarding the CSRD, if Omnibus is adopted, it will be simplifying reporting and postponing the implementation of the Directive. Also, the scope of the directive will be reduced by 80%, as only companies with over 1,000 employees will be required to issue an ESG report. For the rest of the companies, voluntary standards will be adopted in due course.

What are the next steps?

The European Commission has submitted the proposals to the European Council and Parliament for their consideration and adoption. The process could take from several months to years.

Should companies stop their ESG efforts?

ESG does not start nor stop at compliance with the CSRD. Solid ESG practices bring many positive returns to companies with tangible effects on their bottom line. Companies with solid ESG practices have access to sustainability-linked loans with better interest rates, are better positioned to attract and retain talent, and have a more loyal customer base. In addition, current and prospective investors of a company are looking into ESG reports to inform their risk management practices, provide them insights into management stewardship of ESG risks and opportunities, and evaluate the long-term value of an organization.

Below is a comparison between the existing legislation and the proposed amendment: